{kind=link}

Planning for retirement is not just about setting aside money; it is about building a secure future through thoughtful action at every stage of your career. As life changes and your career evolves, so should your retirement strategy. Businesses, individuals, and families can benefit by understanding the crucial steps to take at each phase of this journey. With valuable resources like retirement planning services for businesses, you can ensure you are on a path that fits your needs right from the start.

Whether you are just entering the workforce or about to retire, developing and following a personalized retirement roadmap is key. Early decisions can make a significant difference in your long-term security. With a structured plan, you can adapt to challenges such as economic shifts, unexpected health expenses, and changing workforce trends.

Retirement planning is not a one-size-fits-all process. It changes as you move from your twenties through your fifties and beyond. The most successful retirees are often those who took the time to define their goals, explore their options, and pivot as necessary. Establishing early habits and maintaining flexibility are both essential as you prepare for your future financial well-being.

Modern retirement planning involves decisions about accounts, investments, and spending habits. Staying informed about trends and strategies, and seeking professional guidance when needed, can increase your chances of long-term success. According to a Forbes article on increasing retirement savings, starting early and adjusting along the way are the keys to thriving in your retirement years.

Table of Contents

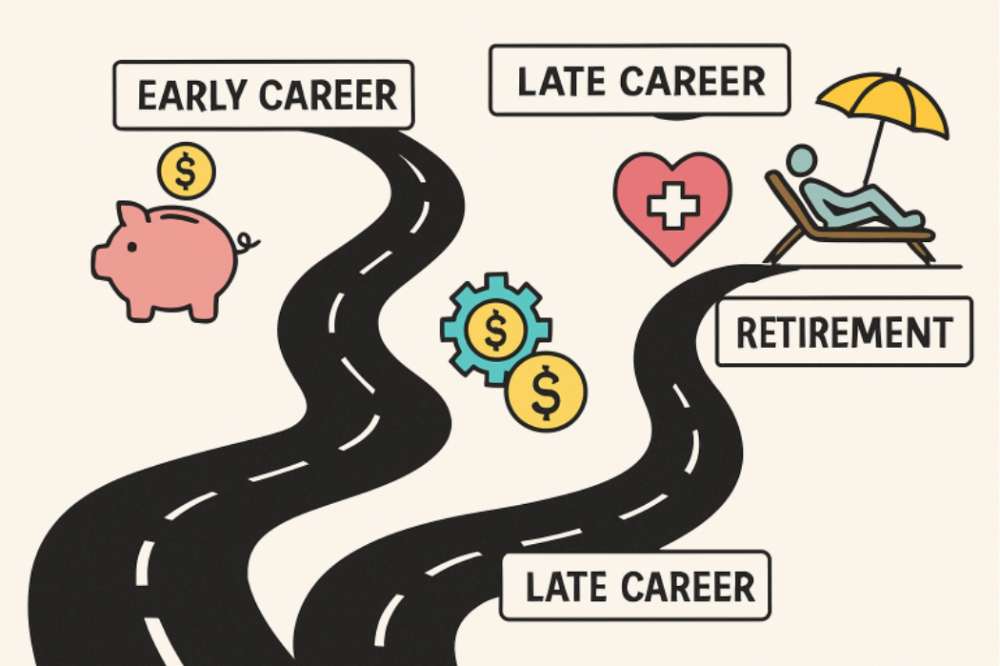

Early Career: Laying the Foundation

Getting started early is one of the most significant advantages in retirement planning. At this stage, your focus should be on building good financial habits and protecting against future uncertainties. Even if you feel like there is not much to save, beginning now pays off through the power of compound interest.

- Start Saving Early: Allocating a portion of each paycheck to your retirement account gives your earnings time to grow and compounding to take effect. Even modest, consistent contributions are better than waiting for the perfect moment to start.

- Utilize Employer-Sponsored Plans: Joining a 401(k) or a similar program means you can benefit from employer matching funds. This is an opportunity to double part of your contribution at no extra cost to you.

- Establish an Emergency Fund: Setting aside savings for emergencies shields your retirement funds from unexpected withdrawals. Typically, three to six months of living expenses is a wise goal.

Surveys indicate that individuals with written financial plans are over 60 percent more confident about their retirement outlook. Putting your plan on paper gives clarity and helps track progress over time.

Mid-Career: Building Momentum

Your thirties and forties are often your peak earning years. This is the time to boost savings, refine your portfolio, and set more specific retirement goals. It is also when competing demands, like mortgages, children’s education, and aging parents, can strain your finances, making diligent planning even more critical.

- Increase Contributions: Aim to dedicate 15 percent or more of your gross income to retirement accounts, scaling up as your income increases with your career.

- Diversify Investments: Ensure your savings are spread across stocks, bonds, and other assets. This helps balance the potential for growth with the stability needed to help weather market volatility.

- Consider Catch-Up Contributions: As you approach age 50, take advantage of increased IRS contribution limits to make up for any shortfalls or to accelerate your savings.

It is also essential to revisit your retirement goals regularly and adjust contributions or investment choices as circumstances change. You may also want to consult a financial advisor for a portfolio checkup and to stay ahead of any investment pitfalls.

Late Career: Preparing for Transition

In the last decade before retirement, planning shifts from growing your nest egg to preserving it. The focus moves towards setting a realistic retirement date, understanding your future spending needs, and preparing for healthcare expenses.

- Review Retirement Goals: Re-examine your estimated retirement age, expected lifestyle costs, and whether you are on track for your targeted savings goals.

- Plan for Healthcare Costs: Research Medicare, long-term care insurance, and other ways to limit out-of-pocket healthcare costs, which can be a significant expense in retirement.

- Develop a Withdrawal Strategy: Creating a plan for how much to withdraw from which accounts, and when, can help minimize taxes and ensure your savings last.

Expert advice often highlights the importance of comprehensive planning at this stage. A proactive approach can help you make the most of your resources when the time comes to retire.

Retirement: Managing Your Resources

Once you are retired, the focus is on making your savings last and keeping pace with the cost of living. Careful monitoring and wise investment choices are still required for long-term financial health.

- Monitor Spending: Keep a close eye on your expenses to avoid overextending your resources and to maintain flexibility in case unexpected costs arise.

- Stay Invested: Maintaining some exposure to growth-oriented investments can help guard against inflation and provide continued income.

- Plan for Required Minimum Distributions (RMDs): Learn about mandatory withdrawal rules for retirement accounts to avoid penalties and tax headaches.

Periodic reviews of your retirement strategy make it easier to adapt as needed, especially when life circumstances or market conditions change.

Common Mistakes to Avoid

Even savvy savers can stumble. Avoid these frequent retirement planning errors:

- Delaying Savings: Waiting too long to start means missing out on the powerful effects of compound growth.

- Underestimating Expenses: Failing to plan for healthcare and day-to-day costs can lead to significant budget shortfalls.

- Ignoring Inflation: If you do not adjust your expectations and investments for inflation, your purchasing power may decline over time.

Creating and maintaining a sound savings and investment strategy puts you in a strong position to enjoy retirement on your own terms.

Conclusion

Retirement planning is not a one-time task but a lifelong journey. By staying proactive at every career stage and adapting when necessary, you build not only wealth but also peace of mind and readiness for the next adventure in life.